How tax cuts could boost your borrowing power

What is your borrowing power and how might the tax cuts help? Let’s investigate.

It’s likely you’ve heard of the Stage 3 tax cuts. After all, they’ve featured in the media a lot over the past few years. And now… finally… they’re here! July 1, 2024 saw the changes come into effect for 13.6 million tax-paying Australians.

Of course, tax cuts have far-reaching implications that can affect the economy in a number of ways. But what will their impact be on the Australian property market? And, more importantly, how will they impact you?

In good news for aspiring homeowners, we believe there’s potential for the tax cuts to increase your borrowing power. That means you can get into your next new home sooner!

Let’s take a closer look at how you can maximise the benefits of the tax cuts to boost your borrowing power.

What are the 2024 tax cuts?

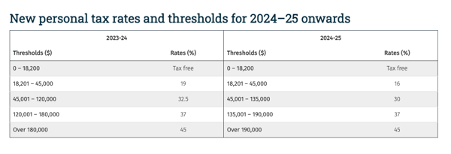

The Stage 3 tax cuts were originally announced in the 2018-19 Budget by then-treasurer Scott Morrison. They were broken into three stages across several years. Stage 1 came into effect on July 1, 2018, Stage 2 on July 1, 2020 and of course Stage 3 this year.

Stage 3 introduces new personal tax rates and thresholds for Australians, which puts more Australians into lower tax brackets, and has lowered the median tax rate from 32.5% to 30%.

Source: treasury.gov.au

For many Australians, your tax cut will make a real difference in your take home pay. For example, if you earn $84,000 in taxable income, you’ll get an annual tax cut of $1,779. You can estimate your own tax cuts on the Australian Government website.

What is my borrowing power?

Of course, tax cuts are great. But if you’re an aspiring homeowner, you’re probably interested in how this will impact your borrowing power. Your borrowing power, also known as borrowing capacity, is the amount a bank or lender will loan to you.

When asking, ‘what is my borrowing power’, the answer will depend on a number of factors. These include your after-tax income, current debt, deposit amount, expenses and more. It will also depend on the lender you’re considering borrowing from, as they’ll have their own factors to determine whether or not you’re a good bet to lend to.

The Stage 3 tax cuts could increase your borrowing power, helping you get into your new home sooner.

What is my borrowing power with the tax cuts?

The Stage 3 tax cuts should mean you’ll pay less tax each year. This of course means more take-home pay in your pocket.

As mentioned above, your after-tax income is one of the factors that lenders will base your borrowing power on. So in a nutshell, a higher after-tax income should result in greater borrower power.

If you’re wondering what my borrowing power after the tax cuts is, you can estimate this in two steps.

First, use the Australian Government’s tax cut calculator for an estimate of your annual tax cut. Next, use our borrowing power calculator. Enter your income, expenses and debts for a rough gauge of your borrowing capacity. Of course, true results will vary for individual circumstances. It’s a great time to get in touch with our team to see what your options might be!

How to take advantage of the tax cuts

Beyond considering ‘what is my borrowing power after the tax cuts’, there are other ways to benefit from the tax cuts.

Of course, any changes in your household income should always result in a re-evaluation of your budget. We would advise against funnelling the extra income into frivolous purchases. Rather, use it to pay off your debts or build your savings. These both make you a better option for any lender.

If you already have a home loan, you may be able to increase your repayments and pay off your home sooner. Or you could deposit the extra money into an offset account.

Maximise your tax-cut potential

If you’re a working Aussie, there’s a high chance you’ll be affected by the Stage 3 tax cuts. This may be through your take-home pay each week or fortnight. Or it may be when you lodge your tax return at the end of the financial year.

If you want to make sure you’re making the most of your increased take-home pay, we’d love to help. You may be wanting to know what your borrowing power is after the tax cuts. You might be ready to refinance with better options. Or you may wish to create an offset account for your existing mortgage.

Whatever your home loan need, the Lending Loop team has the experience and expertise to assist you. We have access to more than 40 different lenders, so you can be sure we’ll find the right fit for your situation. Our mission is to ensure you’re on track to achieving your financial goals.

Give us a call today at Lending Loop!